During the six-year period from 2017 to 2022, India received cumulative foreign institutional inflows of USD26.6Bn into real estate, a three-fold rise from the preceding six-year period. Foreign investments in India have been on the rise over the last few years as the industry underwent an overhaul, with major structural, policy reforms inducing transparency & ease of business operations, according to Colliers’ ‘India- High on Investors’ Agenda’ report. The report delves into the factors that make India a preferred choice for global investors and how it has stepped ahead of other emerging economies. The report also tracks the recovery & growth of the real estate market and explores opportunities for core as well as alternative asset classes such as Global Capability Centers (GCCs) and Data Centers.

“India’s favorable demographic indicators, deep digital talent pool, developmental government policies, infrastructure advancements and competitive costs have made it one of the top choices for global enterprises, fueling real estate demand in India. The strong economic & business fundamentals are enhancing institutional investors’ sentiments; forging strategic partnerships to expand their portfolios. Office sector saw the highest investments during 2017-22, accounting for about 45% of the total foreign inflows. While investors remain buoyant on office assets, their interest in alternative assets is surging,” says Sankey Prasad, Chairman & Managing Director at Colliers India.

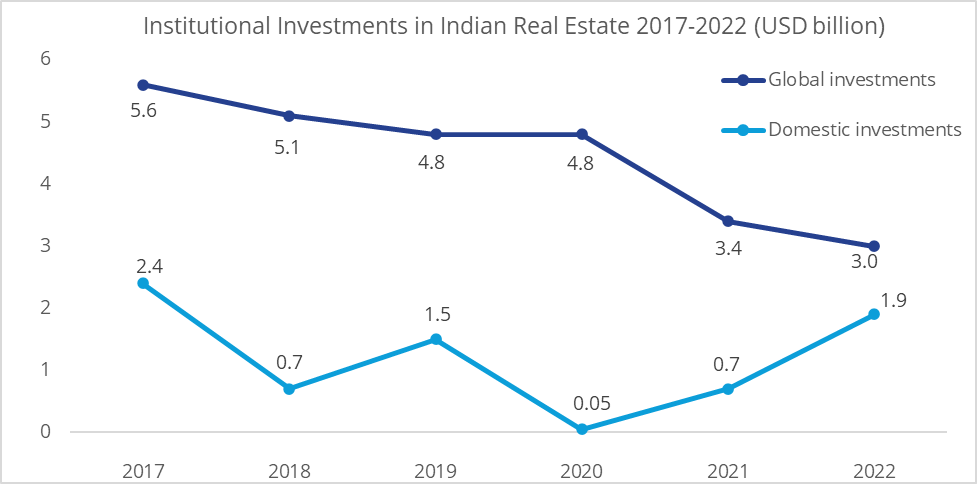

Over the years, global investors have favorably looked at Indian real estate given the resiliency, positive economic outlook, and promising growth prospects of the sector relative to its global peers. According to the report, foreign investments accounted for a sizeable share of 81% of the total investments in real estate during 2017-22. The country’s investor friendly FDI policies, increased transparency in deal structures, and higher investment limits through the direct route have encouraged global investors to invest in India’s real estate sector. Institutional investments in real estate continue to remain upbeat in Q1 2023 as well, rising by 37% YoY at USD1.7 Bn, led by office sector.

“India is on a long-term structural upcycle over the next few years and opportunities galore across spectrum and asset classes in real estate. Over the years, investment in Indian real estate has been getting broader and diversified with newer emerging concepts and themes. India’s attractiveness from manufacturers, occupiers, and investor’s perspective in the Asian Market is on the consistent upswing,” added Piyush Gupta, Managing Director, Capital Markets & Investment Services at Colliers India.

From the perspective of global and APAC investors, the Indian property market currently offers attractive pricing, better valuations, and higher yields. At the APAC level, India has become a preferred investment destination as Indian cities offer higher yields compared to other cities in the region at relatively lower pricing points. Major Indian cities like Bengaluru and Mumbai occupy the 2nd and 3rd positions, respectively, in terms of commercial yield across the APAC region. While Bengaluru leads office yields in the region, Mumbai leads in industrial assets yield. Further, with the Indian central bank pausing the streak of rate hikes, the bond yield is likely to remain range bound. With an expected reversal in the interest cycle over the next few quarters, the yield spread between bonds and real estate is likely to widen, making real estate an attractive proposition for investors.

Core sectors remain resilient while alternatives rise

Investments across various asset classes in real estate sector have seen promising inflows in the last few years. This reflects several opportunities for investors to recalibrate their strategy towards growth sectors. At the same time, investors are recalibrating their portfolio strategy to include new-age growth sectors in order to diersify and fetch higher overall returns. Major investments are already being directed towards alternative assets such as data centers, life sciences etc. While inflows in alternatives are rising, office sector continues to dominate the investment inflows. During 2017-22, office sector accounted for a notable 40% share of the total inflows, reaffirming the resilience and the long-term growth story of the sector. Investors will continue to allocate capital towards greenfield as well as ready to move quality office assets through large platform deals, with greater preference for sustainable assets.

Foreign investments in industrial assets also have been on the rise. Foreign investments constituted 87% of the total investments received in industrial and warehousing during 2017-22 period. Industrial sector is witnessing consistent growth owing to increased opportunities in manufacturing, favorable government policies and growth in E-commerce, leading to a significant amount of investible assets in the region.