The festive season is underway, and it is that time of the year when consumers loosen their purse strings to welcome abundance into their homes. From apparels, electronics and automobiles to gold, home furnishings and property purchases, consumers are driving sales across sectors. Residential real estate in fact is having one of the best performing years in the past decade.

Now, to understand the probable trajectory of Indian real estate, it is imperative to look beyond the current trends. Does the repo rate and consequential home loan interest rates play a significant role in influencing residential segment activity at the macro-level. Is it affordability, which provides tailwinds to the housing sector momentum or is it more of policy decisions which shape the contours of residential activity in India. Factoring in a historical evaluation is likely to provide potential clues for market analysts, homebuyers and investors in Indian residential real estate.

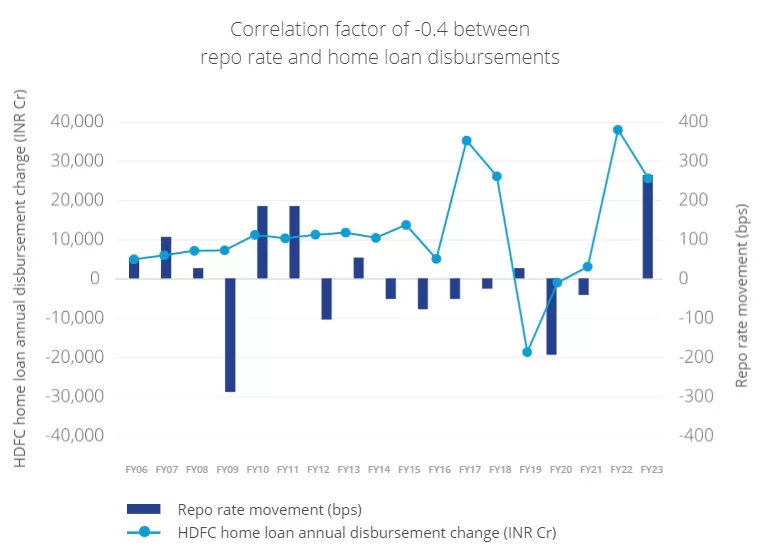

Repo rate movement has low correlation with housing disbursements at the macro-level

While home loan EMIs do have a role in swaying the home-buying behaviour at the end-user level, the impact is more pronounced on fence-sitters as compared to aspirational buyers. Consumers understand that repo rate and hence EMI quantums are quite volatile over the tenure of a home-loan. Homebuyers are more likely to alter the location, construction stage, ticket and unit size, developer preference and housing society amenities, rather than hasten or delay the purchase decision itself. Contrary to popular perception, a low correlation between annual home loan disbursements of HDFC (one of the systemic banks having a significant home loan book) and repo rate clearly indicates that interest rates comparatively have low bearing on housing activity in India, especially at the broader industry level.

Regulatory measures bolster the upside and cushion the downside

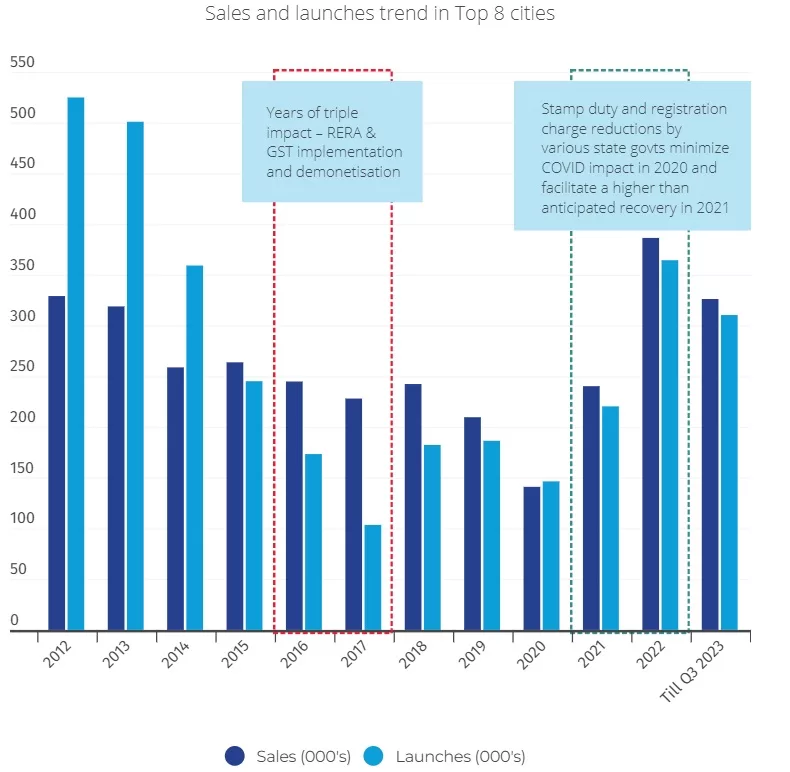

Top 8 cities include Ahmedabad, Bengaluru, Chennai, Delhi-NCR, Hyderabad, Kolkata, Mumbai, and Pune

Although the impact of interest rates on the overall housing market activity seems relatively low, regulatory measures have a far greater impact on demand and supply side dynamics. For instance, 2016 and 2017 were two consecutive years of drop in residential sales and launches – the dip in developer confidence and consumer sentiments can be attributed to three landmark events – RERA & GST implementation and demonetisation in a very short period of time. Similarly, of all segments, in the initial days of the pandemic, most experts believed that residential real estate would face the maximum brunt. However, various state governments stepped in with reduction of stamp duty and registration charges by up to 2%. Such limited period reductions along with extension in construction timelines helped the housing market to remain buoyant in 2020 and embark on a steep V-shaped recovery trajectory in 2021. The momentum was carried forward in 2022 and 2023, the years have witnessed significant traction in both sales and launches, despite healthy increase in average prices across most Indian cities.

Affordability – The pivotal element in housing market activity

Average prices are representative of Mumbai, Delhi-NCR, Bangalore, Ahmedabad, Lucknow, Kolkata, Chennai, Jaipur, Kanpur and Kochi

Over the last decade (FY13 vs FY23), while average housing prices in India have increased by around 90%, income levels captured by per capita income have increased by almost 150%. In fact, the uneven growth in housing prices and income levels is substantial, if we compare early 2000s and today. Hence, affordability of home purchases in the country, measured by a factor of average buying price of a 1000 sq.ft. house and annual per capital income, has improved significantly from 50-60 in the 2000s to below 40 currently. With the influx of MNCs and success of service sector in a post-liberalised Indian economy, affordability and hence residential sector activity has always been on the growth course, even in the face of crises such as dot-com bubble, 2007-08 financial crisis, NBFC sector crisis and the more recent COVID-19 pandemic.

Last quarter to propel momentum ahead

The festive season in Q4, marked by willingness of homebuyers to finalise property purchase decisions and developers offering attractive discounts and freebies, has historically provided the final push to residential activity within a year. Almost 40% of the annual residential units sold achieve closure in the last quarter. Both sales and launches in 2023, till the third quarter, have come close to 2022 levels. Considering the historical festive trend, 2023 is likely to witness 20-30% higher sales as compared to 2022.

Residential real estate momentum is likely to continue in 2024 as well. The Indian housing market will continue to derive strength from a multi-decadal high affordability and the innate sentimental value of owning a house. Transparency and better adherence to regulatory disclosures, all brought in by RERA, have reduced ambiguity with respect to real estate transactions in the country to a large extent. The pandemic has accelerated the adoption of technology in many aspects of life, including real estate. In the next few years, the homebuyer is likely to get increasingly adept with smart homes, virtual tours, and digital transactions. Evolving construction technologies and environment-friendly practices are anticipated to provide further credibility to sustainable housing soon.

About the Author:

Suryaneel Das, General Manager | Research, Colliers

Suryaneel has close to a decade of experience in research, consulting, advisory and credit assessment across varied segments including real estate, renewable energy, roads, construction and infrastructure sector. All throughout his professional career, his core skill sets have been sector research, advisory, consulting, credit appraisal, risk analysis, financial modelling, client handling, management discussions and structured finance.