Industrial & warehousing demand across the top five cities was stable during H1 2023 with 11 mn sq ft of leasing, compared to the same period last year. Delhi NCR continued to lead demand with 25.0% share, closely followed by Mumbai at 24.6%. While most of the cities saw a single-digit change in demand, Mumbai witnessed a notable 28% YoY increase in leasing during the first half, largely driven by expansion from players in 3PL sector. Despite the global economic headwinds, the industrial and warehousing sector is seeing steady growth backed by rising capital investments, manufacturing output and government policy enablers.

The consistent trend in leasing was primarily driven by 3PL operators, accounting for 37% of total leasing during the first half of 2023 followed by FMCG and Engineering firms with a share of 12% and 11% respectively.

Trends in Grade A Gross absorption (mn sq ft)

| City | H1 2023 | H1 2022 | YoY Change |

| Delhi NCR | 2.8 | 3.0 | -8% |

| Mumbai | 2.7 | 2.1 | 28% |

| Pune | 2.4 | 2.7 | -9% |

| Chennai | 1.7 | 1.7 | 1% |

| Bengaluru | 1.4 | 1.5 | -4% |

| TOTAL | 11.0 | 11.0 | 0% |

Source: Colliers

Note: Data pertains to Grade A buildings

Trends in Grade A Supply (mn sq ft)

| City | H1 2023 | H1 2022 | YoY Change |

| Delhi NCR | 3.7 | 5.1 | -27% |

| Pune | 2.3 | 1.6 | 48% |

| Chennai | 2.0 | 2.2 | -11% |

| Mumbai | 1.6 | 1.8 | -11% |

| Bengaluru | 1.1 | 1.2 | -10% |

| TOTAL | 10.7 | 11.9 | -10% |

Source: Colliers

Note: Data pertains to Grade A buildings

“While 3PL continues to lead demand, leasing by FMCG and engineering firms across the major markets in India witnessed a significant rise during the first half of 2023. Notably, demand from E-commerce rose 68% YoY, after a lull in the last few quarters. The overall demand for the industrial and warehousing market has been bolstered by various factors, including increased production capacity, strong government policy support and inclusion of more automated and process-driven manufacturing. While 3PL players are likely to dominate demand, we expect strong & steady momentum in leasing from other segments as well,” says Vijay Ganesh, Managing Director, Industrial & Logistics Services, Colliers India.

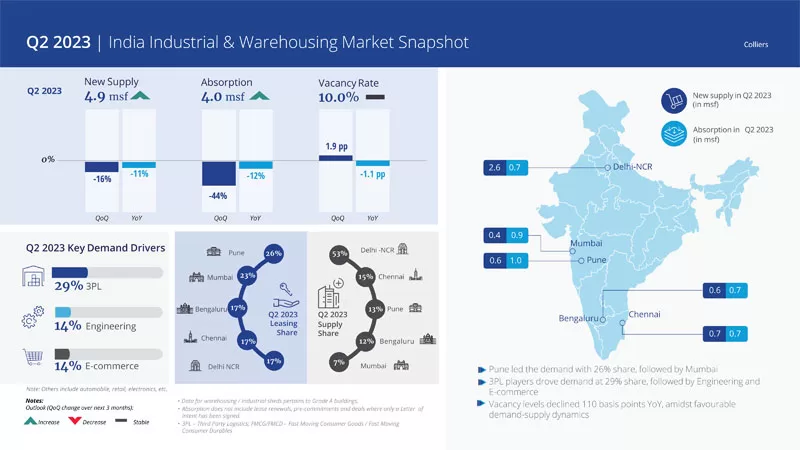

Amidst steady demand for quality Grade A warehousing spaces, vacancy levels during the first half of the year dropped by 110 basis points (bps) to 10.0%. This period saw fresh supply of 10.7 mn sq ft, a 10% dip YoY, as developers remained watchful on the evolving demand scenario. During the six-month period, the second quarter saw some moderation in demand with 4.0 mn sq ft of leasing. Pune led the demand during the quarter with 26% share.

“Despite global economic headwinds, India’s industrial & warehousing market remained resilient in the first half of the year. Buoyed by favorable demand-supply dynamics, vacancy levels dropped by 110 bps to 10%. Resultantly, overall rentals inched upwards marginally. India’s high performance economic indicators are displaying encouraging signs of improvement, with steady gains in manufacturing output & investment. This augurs well for the sector in the short to medium term,” says Vimal Nadar, Senior Director & Head of Research, Colliers India.

Trends in Grade A Vacancy rate (%)

| City | H1 2023 | H1 2022 |

| Delhi NCR | 14.1% | 16.1% |

| Mumbai | 12.1% | 11.5% |

| Bengaluru | 6.8% | 6.1% |

| Chennai | 5.6% | 6.3% |

| Pune | 5.5% | 8.9% |

| Pan India | 10.0% | 11.1% |

Source: Colliers

Note: Data pertains to Grade A buildings

Leasing by FMCG players surged three-fold during H1 2023

While 3PL players drove demand during the period, the share of leasing by 3PL players dipped to 37% from 53% in H1 2022. At the same time, leasing by FMCG players experienced an impressive three-fold rise as they expanded their presence in key markets such as Delhi NCR and Mumbai.

Large sized deals account for 75% of the total leasing

During H1 2023, large deals (>100,000 sq ft) accounted for about 75% of the demand. Amongst these larger deals, 3PL companies contributed to a lion’s share, followed by FMCG and Engineering players. Mumbai followed by Pune dominated the chunk of large-sized deals across the top five cities.